16. April 2016

The Clockmaker - Define your own DNA in analysis

I'll come clean and admit that I have "a thing" about watches. I can't hide it. I am a WA (and in case you're wondering that is: a Watch Aficionado). I like watches. But the thing is that I have a thing about lots of things. I also have a thing about good chocolate. Maybe "having a thing" IS my thing? (by the way, did you see how I managed to put quotation marks, capitals and indented in one sentence, whoa). Anyway, I'm getting sidetracked here (again). We were talking about watches. In three words - I like 'em. And I'm going to describe your inner Clockmaker today.

The theme of this post is that I'm trying to describe three different types of analysts:

The Historian

The Gunslinger

The Clockmaker

I have already written about the Gunslinger. The idea is that you end up understanding yourself and your own particular style or DNA of analysis/trading based on these three types. So you get to know and define your own style. All it takes is that we go through the three archetypes, and then you can blend these three colours into your own mix. It's like the colour in your living room where you make your own particular blend. The only difference is that you don't make one final mix of the three colours and paint it on the walls, but you sort of evolve the colours along the way, adding and subtracting as you yourself evolve. So with this post no. 2 let's take another step in defining your own sweet spot, your own unique DNA.

The Clockmaker is a Fundamental Analyst. You already know what that is, but to sum it up in a few words it is an analysis of the things that affect a price. For a commodity the things that affect its price is the state of the economy, supply, demand, inventories, seasonality, currency, macro economy, speculators and so on. For a company the thing that affects its stock price is the economy (GDP growth, regional growth), its industry (the trend of the whole industry group), the company itself (its assets, liabilities, earnings, its brand value, cash flow, management team etc.) and its competitive advantages and so on. Whew, what a lot to juggle with! And you have to make sense of all this (that means not only analysis but also synthesis).

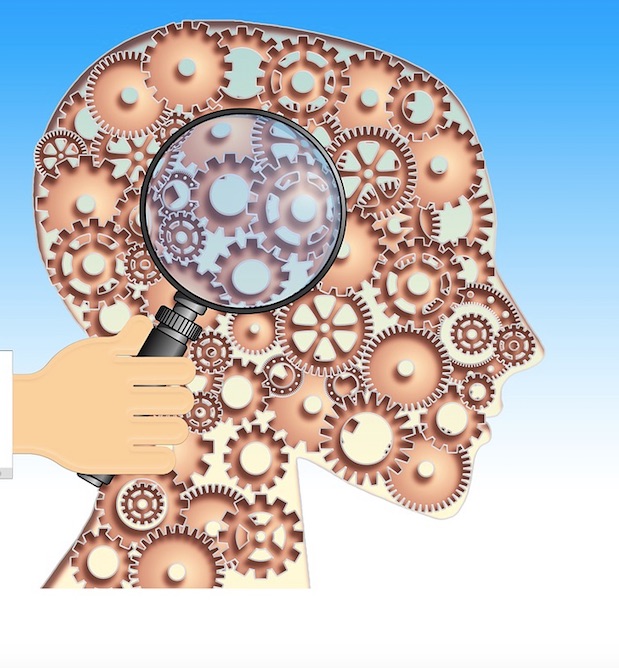

Start by having a look at picture no. 2. This is how a Clockmaker thinks and analyzes - with gears, springs and levers. The Clockmaker is sitting at his immaculate desk with a magnifying glass, carefully seeing how each intricate part of this watch works and interacts with other parts. This wheel turns and interacts with that lever. Inside a watch you only have the gears and wheels that are necessary. No more or no less. And they have to fit together. And if something doesn't work, you can find the problem by using logic. There is also a cyclical timing element. You are aware of the cyclical nature of seasonality and the fact that supply surplus turns into supply deficit, and then back to surplus again and suddenly something happens to make it a deficit again. Back and forth. 12 o'clock is different than 6 o'clock. But if you're at 6 o'clock now, the whole thing is slowly turning back to 12 o'clock. So the watchmaker understands that this is a pendulum continually working it's way between surplus and deficit. The GDP growth is also cyclical. There's a clock-like quality to most things. And all the moving parts in the watch are earnings, P/E ratios, cash flow and a whole bunch of other information, levers and gears - all interconnected. And every wheel has its function in the watch. You cannot take ANY part out of the watch, or it will stop working. Hint: Take a look at my own watch on the right and see how the pieces fit together. So you need to be a good watchmaker to make all of this fit together. It should "keep time", i.e. be properly weighted and assembled.

Fundamental analysis is actually not a coherent analysis as they try to make it out. The analysis is split into two very different parts:

Quantitative fundamentals: This is left brain thinking with mathematical precision and gears. Cause and effects. Real world data.

Qualitative fundamentals: This is right brain thinking. This is about assessing what comparative advantages this brand has over another, what strategic advantages this company has over another. And how this brand will develop into the future. There is no absolute result in this. This is subjective and depends on the ability of the analysts to think strategically, comparatively and laterally.

The part about Qualitative is a real bonus for me, because that means that Fundamental analysis is not objective. They do try very hard to make themselves out as being objective - as opposed to Technical analysts that they regard as Gunslingers. But it turns out that a huge chunk of fundamental analysis is Qualitative and without any objective truth, only subjective assessments. Boy, does it feel good to throw that in their faces. Let's just repeat that: Fundamental analysis is to a large degree subjective, with only a part of it being objective. That's the same with Technical analysis, i.e. no difference. Ha!

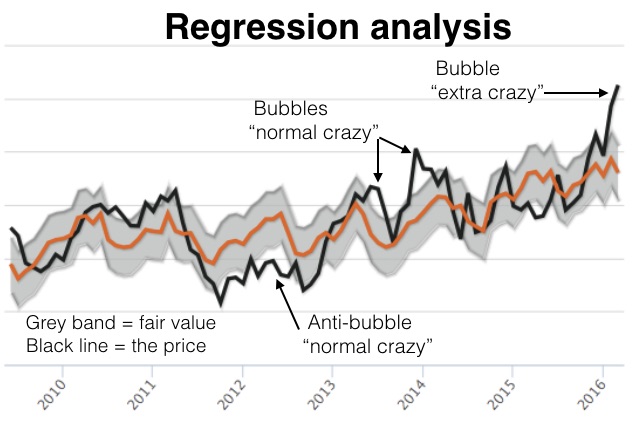

The Clockmakers most difficult challenge is that he's required to not be strictly logical all the time (which sounds strange). He has to adapt his thinking to the fact that society in general has a tendency to overreact. Sometimes prices get too low or too high. You see this when you make a regression analysis (and I count this as just a part of the Fundamental analysis). This will tell you the fair price level. But sometimes prices are "too high" compared to a fair level, and sometimes they are "too low". I call that bubbles and anti-bubbles.

Over the years every market consistently experiences overreactions. The fundamental analyst has to recognize that the market is in a bubble or anti-bubble (unsustainable price levels) - but that is not enough. Oh no, that would be too easy. Even with a price that is too high, the bubble can be blown higher. So we have to compare previous bubbles to the current bubble to see if “things are more crazy than normal”. So we are now measuring current craziness to previous craziness in order to determine if prices are “extra crazy” now, or just “normal crazy”. Weird, isn’t it? But that's part of the analysis. The chart on the right shows such a regression analysis.

So what makes a good Clockmaker?

Intelligent overview. There's truly a lot of data to keep track of (earnings, macro economy, cash flow and on and on). So many gears. But it's not enough just to collect all the gears and wheels. They have to be fitted together, so that they turn. And you cannot miss just one gear. A good Clockmaker has a good intelligent overview and knows how to fit the pieces together.

Effect. A good Clockmaker should know what effect comes from a certain development in a fundamental. The effect comes from understanding how the market previously has reacted to similar fundamental developments - but also putting it into present context. You have to assign Weight to every fundamental. And you have to assign Time influence to every fundamental (whether it has an effect right away or with a delay). What lever will affect what gear? And he also has to be pragmatic when there is no available data, or when the data is questionable. He then has to be able to "connect the dots". And you also have to factor in the human side of how people will react to this news - first as anticipation and then as real news. A good Clockmaker understands what effect a development will cause.

Pragmatic. The Clockmaker has never seen a "true number". Every number he has ever seen has been flawed. Take any number whatsoever, be my guest. That is the topic of another post in itself. The best description I have heard is Garbage in - Garbage out. That also applies to the qualitative part (but here your assessment can be the garbage, not the data). So the Clockmaker cannot sit with precise gears. He has to be able to cope with flawed data, inconsistent data and missing data, as well as with data that is suddenly being revised years back in time. On top of this he also has to be pragmatic enough to know when to stop. I've seen analysts going overboard in details upon details, and every one of them are fascinating and multi-layered. And at one point they totally lose the overview of what it all means and what the total outcome is. So the Clockmaker has to assess data with a pragmatic view, and also know when to stop.

He has a visionary assessment. Due to the Qualitative part of fundamental analysis it is imperative that the Clockmaker has a right brain mode with a keen and visionary understanding of how a brand or company or commodity will develop - in comparison to competitors - due to its inherent qualities. Knowing that this assessment can never be proven, he still has to hit it right and be confident in his assessment.

Some of the qualities I mention above may appeal to you more than others. Use them in your own sweet spot. But also recognize the parts that you don't have (and are reluctant to start because of the work involved). You don't have to be a specialist in everything, but a little can sometimes get you far. Then when we have completed post no. 3 we can start to put everything together, so that you can define your own unique DNA.

This is the Clockmaker in you. It's a challenging, strategic and jigsaw-puzzle-collecting work, but rewarding. It's like when you as a boy disassembled your alarm clock and saw how things work, how everything was functioning (eh, did you manage to put it all together?? I couldn’t make the alarm clock work again). It's a salute to your sense of curiosity about how the world works.